By Kevin D. Williamson

Monday, August 25, 2025

We should have eaten our spinach.

Nearly 20 years ago, I started writing a column for National Review called “Exchequer,” with a focus on fiscal policy, debt, and

deficits. A point I frequently returned to—and frequently return to still—is

that dealing with our national debt problem and getting the U.S. government’s

finances back onto stable footing is something that will be easier to do the

sooner we start and more painful to do the longer we wait, especially if we put

off reform until we are in a fiscal crisis of some kind, which is what

Washington seems dead set on doing.

I was—and am—what my friend Larry Kudlow calls an

“eat-your-spinach guy.” Kudlow and other sunny optimists, such as Arthur

Laffer, are not big on eating spinach. They are big on ordering dessert first,

counting on tax cuts and other incentives to goose the economy to such an

extent that GDP growth does the hard work for us—what I have referred to at

times as “naïve supply-side” economics. When it comes to diet, eating dessert

first will indeed tend to make you grow (like it or not), but economic growth is,

alas, a little more difficult to goose.

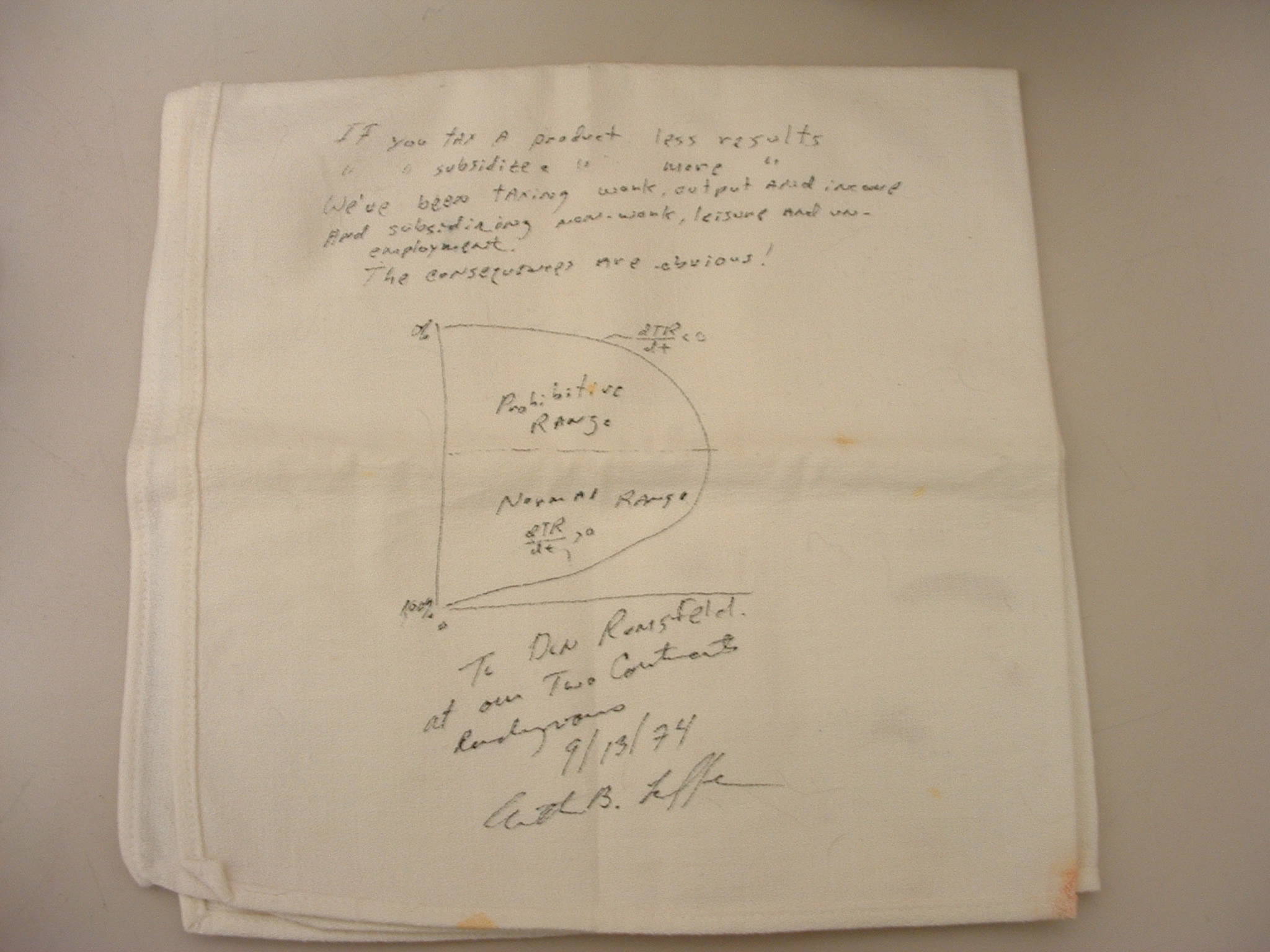

While Laffer and politicians enamored with his famous

curve are correct

to observe that growth effects from tax cuts may in

some circumstances mean that $1 in on-paper tax cuts does not actually produce

$1 in real-world lost revenue, it is not the case, as the naïve supply-siders

have promised from time to time, that tax cuts are typically revenue-enhancing

in the context of a modern market economy. A $1 tax cut may end up losing

the Treasury only 82 cents (or whatever; these numbers are purely for

illustration) in revenue, but $1 in tax cuts does not “pay for itself” and then

go on to produce an extra 22 cents (or whatever) in additional tax receipts—typically: Laffer

is correct in arguing that there are circumstances in which a tax cut can be

revenue-enhancing in a meaningful way (imagine cutting investment-income taxes

from 99.9 percent to 20 percent and the effect that would have on both

investment and tax compliance), but those circumstances do not seem to be

found, or at least do not seem to be often observed, in the U.S. economy.

{kind=link}

As is often the case, one of the problems we run into is

using the wrong point of comparison: Tax revenue has sometimes increased

following tax cuts, but gross receipts normally trend reliably upward in the

U.S. economy, simply because the U.S. economy grows, sometimes rapidly and

sometimes modestly, except during those rare (but regular) periods when it is

in recession. Lots of things contribute to growth or lack of growth—tax policy

can be one, but it isn’t the only one or, in most cases, the most important

one. (Attributing 100 percent of U.S. economic growth to the tax policies of

this or that presidential administration or Congress is unserious and

intellectually dishonest.) The relevant point of comparison is not between tax

revenue before and after the tax cut, but between tax revenue with the

tax cut and what it would have been without the tax cut—which is an

unobservable counterfactual, one that we can model or estimate but cannot

directly measure per se.

(We run into the same problem with the debate about the

effect of minimum-wage laws on employment; comparing employment, total wages,

etc. before and after the change does not actually tell us anything very

useful; the relevant comparison is between what actually happened in the job

market and what would have happened absent the policy change, which is, again,

not directly observable.)

What the naïve supply-siders are actually acting on is

not some rigorous economic theory based on Laffer’s work, but what supply-sider

Jude Wanniski called the “Two Santa Claus Theory,” which is not a theory of economics

but a theory of politics: Nobody votes for Scrooge, and, so, when it

comes to bribing Americans with our own money, the Republicans need something

to compete with the Democrats’ spending giveaways. Tax cuts filled that

political role splendidly until Republicans had so much success with them that

tax cuts lost their political juice, because a majority

of federal tax revenue is now extracted from a small

minority of high-income taxpayers, one whose total federal income-tax burden

far exceeds its share of total income.

Growing our way out of hard choices is a nice idea. But

the fact is that there is no fat guy in a red suit coming down the chimney with

a sack full of budget-balancing goodies. I will be sad when the day comes when

my children stop believing in Santa Claus—but I will be grateful when the day

comes when my conservative friends do.

During one memorable conversation on Kudlow’s old CNBC

show many years ago, he hit me with a very bold claim: that he and other

like-minded eat-dessert-first guys could, if given the chance, get the economy

back to Reagan-era levels of GDP growth—and keep it there on a sustained basis.

“I did it before, and I’ll do it again,” he thundered.

That was cable television, and he was being entertaining, of course—though

Kudlow was a policy bigwig at Reagan’s Office of Management and Budget, he does

not actually believe he was personally responsible for the booming economy of

those years. But he is also a true believer. As it happens, history handed us

an opportunity to test Kudlow’s confidence, and he became director of the

National Economic Council in the first Trump administration, where he was

joined by many like-minded economic thinkers (and a fair number of utter

crackpots). The verdict is in, the jury is unanimous, and there is no appeal:

The eat-dessert-first guys have hosed us good. You guys

really should have eaten your spinach.

Wind back the clock 15 years or so. In 2010, the U.S.

economy was recovering from the financial crisis and the Great Recession.

Average real

GDP growth during the Barack Obama years (please apply

the usual caveat about superstitious beliefs involving presidents and economic

performance) was a

relatively anemic 2.3 percent, and the national debt when Obama left office

in 2017 stood at $20 trillion—a shocking number. In 2017, Obama handed

the keys over to Donald Trump—and, through him, to Kudlow et al.—and what

followed during the first Trump administration was … four more years of

relatively anemic 2.3 percent economic growth, with the national debt standing

at an even more shocking $28.4 trillion. Even before the COVID pandemic, the

deficit was growing

during the Trump years, not declining.

Nice going, optimists.

If you really want to put yourself into a

jump-out-of-a-window kind of mood, consider what could have been if the people

in power had listened to us eat-your-spinach guys. Those of you who are old

enough to remember 2010 will not remember it as a period of terrible

austerity—we had a big, fat federal government in 2010, with a lot of big, fat

federal fingers in a lot of pies. What would have happened if we had simply

held the line at the time and kept spending at 2010 levels of $3.45 trillion a

year for the next 15 years? Assuming that tax revenue came in at its actual

historical numbers (and conceding that this is grossly simplified,

back-of-the-envelope stuff) we’d have a very, very different outlook: Not a

balanced budget or a paid-down debt, but an accumulation of only (only!) about

$2.7 trillion in new debt over the next few years, with—the really good

news—the national debt peaking in 2018. The budget would have gone into surplus

in 2019, and the new president and Congress coming into office in 2021 would

have enjoyed a considerable and well-established primary surplus—which, if they

just kept letting my imaginary scenario play out, would have driven the debt

down mightily in the subsequent years.

(In case you are wondering: In order to avoid having the

comparisons distorted by inflation, both revenue and outlays in the above

scenario are in 2009 constant dollars as calculated by the U.S. Treasury. You

can access a whole mess of very interesting spreadsheets detailing revenue and

outlays here.

I’d like to emphasize here that this is not meant as some kind of rigorous

econometric model of what would have happened, only to give you a sense of the

scale of how much easier it would have been if we had started working on the

problem 15 years ago—it’s not like we didn’t know it was a problem then.)

Tax hikes are not my favorite spinach dish, but let’s add

that ingredient into the mix. Would higher tax revenue help stabilize the

national finances? Undoubtedly. From 1996-2001, federal tax collections ranged

between 18.2

percent and 20 percent of GDP, topping out with the sizable budget surplus

of 2000. Those were some pretty good years, economically speaking. (It wasn’t

that the economy was good because taxes were high; it was more the case that

tax revenue was high because the economy was booming.) Taxes dipped below 15 percent of GDP in the wake of the financial crisis, but were

back up to the 18-percent range by the end of the Obama years. The problem is

that federal spending jumped

up from 17.5 percent of GDP in the surplus year of

2000 to more than 20 percent of GDP by the end of the Obama years. If taxes had

held steady at almost 20 percent of GDP, we’d have run deficits of about 0.4

percent of GDP on average instead of the 3.5 percent of GDP we actually

averaged.

And things did not improve from there. The Trump era was

marked by persistently high spending, and not only in the outrageous

COVID-spike year of 2020, when spending hit almost 31 percent of GDP. Spending

barely dipped below 20 percent (and I do mean barely: to 19.9 percent)

in 2018, but otherwise remained above 20 percent of GDP throughout the first Trump administration. Trump-era tax

receipts maxed out at 17 percent in 2021, but mostly stayed closer to 16 percent.

Revenues at 16 percent of GDP and spending at 20 percent of GDP is how you go

broke. Revenues at 20 percent of GDP and spending at 20 percent of GDP is how

you have a government that is fiscally stable, even if a few of us cranky

libertarians gripe about $1 in $5 being hoovered up by Uncle Stupid.

The Puritan in me doesn’t like public debt at all, though

we might have found it expedient to take on a little bit of extra debt related

to COVID or needful military and infrastructure improvements, but these would

be, in the grand scheme of things, eminently manageable—had we put ourselves on

sounder footing back when doing so would have been both politically and

economically easier. Imagine having the world’s largest national economy—one

that is the global center of both technological and financial life—and enjoying

prudent, low-debt, or even deficit-free government with excellent long-term

fiscal prospects. One assumes that this would have had some happy effects on

capital flows, interest rates, and—most important—real investment and

innovation.

What did we get instead? In the first quarter of this

year, federal debt stood at 120 percent of GDP.

Spending is out of control. Entitlements remain unreformed. Needed expenditures

are put off because our finances are under so much pressure from popular

giveaways and, increasingly, from interest payments on the debt that we have

already acquired, which now exceed spending on national defense. We spent more than $1

trillion on interest payments in 2024, and have already spent more than $1

trillion on interest in FY 2025. Our tax code still appears to be the

nightmarish work of a joint committee comprised of Franz Kafka, Hieronymus

Bosch, Otto von Bismarck, and Thurston Howell III. We spend money like a

methhead with an 88 IQ and a PowerBall jackpot that just hit his checking

account.

And for what? What do we have to show for it? Joe Biden

got to spend a ton of money on green-economy nonsense under the pretext of

reducing inflation. Donald Trump got to put his signature on

some COVID-19 relief checks. Warren Buffett’s Social Security benefits were

not reduced.

Hooray.

A couple of years of ugly inflation seems to have been

enough to generally discredit “Modern Monetary Theory,” the beloved progressive

superstition that the U.S. government can run essentially infinite deficits and

engage in essentially infinite spending without ill effect simply because it is

able to borrow in its own currency. Oops. Embarrassing! But we have more than a

couple of years—a couple of decades, in fact—of evidence that Republicans’

strategy of growing our way out of our dire fiscal straits simply does not

work.

Alas, I do not think that people who are content to work

alongside such crackpots as Peter Navarro are capable of being embarrassed by

economic policy, however imbecilic.

If you want to fix the debt, then you have two levers to

pull: One is increasing tax revenue, and the other is decreasing spending. It

is not easy to do, but the basic options are not impossibly complex. We should

avail ourselves of those options while we still have options.

I like spinach. And one good thing about spinach: It’s

cheap.

Wishful thinking, on the other hand, is expensive. And we

cannot afford much more of it.

Words About Words

You know how 3-year-olds ask a lot of perplexing

questions? My oldest boy has questions—lots of them. And the other night at

dinner, over his fruit course (which followed the rice course and preceded the

nugget course), a language matter arose: We call collard greens “greens”

because they are green—but do we call oranges “oranges” because they are

orange, or do we call the color orange “orange” because it is the color that

oranges are? Mojo leaned toward the latter explanation, and, as it turns out,

he is correct.

Orange, that famously unrhymable word (don’t tell Eminem), comes

from the Sanskrit nāraṅga

via Persian, Arabic, and French derivatives, with the word referring to the

tree and its fruit, after which the color is named. If it weren’t for the

fruit, what would we call the color? Perhaps “sunset,” or “carrot,” or

“pumpkin,” or “trump.”

The amarillo tree, on the other hand, is named for the

color: Amarillo is Spanish for yellow. (The Texas city in which I

was born apparently takes its name from the yellowish soil around the stream

where the first Spanish settlement there was planted.) So, it’s the other way

around from orange. The Spanish color comes from the Latin amarellus

and its root, amarus, meaning sour or bitter—one

hypothesis is that the color name was inspired by the yellowy hue of bile, one

English term for which, gall, is related to the English word for yellow.

Our English yellow comes from a Proto-Indo-European root meaning shine.

It is geolu in Old English and related to such words as green, gold,

glow, glitter, gleam, and, as mentioned, gall—variations

on the themes of brightness, yellowness, and glowing.

Many languages have related words for red, mostly

beginning with r- and derived from the Sanskrit rudhiráḥ, meaning bloody or,

simply, red.

Blue seems to have been derived from words that

just mean blue.

Black comes from the Proto-Germanic word for burnt.

White comes from the Proto-Indo-European word for

people who vote for Bernie Sanders.

(No, not really, but have you seen Vermont?)

In Closing

The Trump administration has, no great surprise, targeted

former Trump aide John Bolton, launching a criminal investigation into the

supposed mishandling of classified information. The current director of the

FBI, Kash Patel, put

Bolton on an enemies list he published in a book

called Government Gangsters; Patel is a crackpot and a documented

fabulist. Vice President J.D. Vance says the investigation is “not at all” related to political

considerations; the vice president is a reasonably

well-documented habitual liar and fabulist, one who has gone as far as to

publicly justify his fictitious inventions on the grounds that they are

politically useful. At the top of the Trump administration is Donald Trump, who

is surely the most prodigious liar in the history of American public life. At

the top of the Justice Department is Pam Bondi, who manufactured

fake evidence files in the Jeffrey Epstein matter to

use as props.

I do not know John Bolton well. What I do know of him

suggests that he is a man of integrity and generally good judgment, although he

had the poor judgment to go to work for the Trump administration the last time

around and has suffered the reputational diminishment inevitable in doing so. I

am certainly inclined to trust him more than any of the grotesques, fools, and

miscreants who have his name on their public or private lists of enemies.

I wish John Bolton well and would be surprised to learn

that he had done anything malicious or irresponsible in his public duties. But

his current travails are a reminder that there is no honorable way to serve in

a Trump administration, and that the price of doing so can be very, very high.

You lie down with dogs, you get up with fleas.

No comments:

Post a Comment